More pain to come before we beat the bug

Hi

The good news is that, according to Bloomberg…

“China could be just days away from declaring it has no new cases” of coronavirus.

That’s if we believe State figures, of course.

Since the start of the virus story, official numbers coming from the Chinese authorities have been fudged, misreported and rejigged.

So much so that it’s become the norm to take them with a large pinch of salt.

We’ll have to wait and see whether indeed news breaks that there are zero new cases.

Now it’s the world’s problem

More importantly, even if China is past the peak, pretty much everywhere else in the world, things seem to be getting worse.

According to the Johns Hopkins University COVID-19 Tracking Map, confirmed cases (as of Thursday evening) are 128,343 with 4,720 deaths worldwide.

- Italy has lost 1,016 lives to the bug and is in lockdown to stop it spreading further;

- Almost every European country has closed or restricted schools;

- Sporting events are being played behind closed doors or cancelled;

- Major international conferences and festivals are being axed or postponed;

- President Trump has banned flights from certain European countries from entering the US;

- The World Health Organisation has finally admitted this is a pandemic… not just a bunch of epidemics;

- Angela Merkel predicts up to 70% of the German population could contract the virus;

- High profile people including politicians and film stars have come forward to announce they have contracted the disease.

But here at Monkey Darts, our brief is money and markets.

And as if the threat to health wasn’t ominous enough, the effect on financial markets and to the global economy is devastating.

It’s pretty much as we would expect: stocks are getting hammered.

Meanwhile, gold – the ultimate safe-haven asset – is holding up, although as we’ll see in a moment, amid the “rush to cash”, it’ too has felt its own downward pressure.

So, what’s the problem?

Containing the virus kills economic activity

Ben May, head of global macro research at Oxford Economics:

“From an economic perspective, the key issue is not just the number of cases of COVID-19, but the level of disruption to economies from containment measures.”

Globally, governments have seen the success with which China has managed to contain the spread of the virus by locking down entire regions.

Now we’re seeing similar strategies adopted in other countries around the world. Italy was first, but expect to see many more follow suit as they try to keep the virus from spreading.

But shutting down economies comes with a cost.

First, to their own economy and population. But also, to the economies of other countries that rely on their exports.

For example, Fortune reports on how China’s restriction on factory output leads to knock-on effects in the US:

“Nearly 75% of companies are seeing capacity disruptions in their supply chains as a result of coronavirus-related transportation restrictions, according to an Institute for Supply Management survey published Wednesday.

“This is strong warning sign that COVID-19—which was ruled a pandemic by the World Health Organization on Wednesday—is weighing down the global economy.”

China is a huge source of both components that go into products and certain finished products themselves.

Goker Aydin, a business analyst from Johns Hopkins University explains:

“The longer plants in China sit idle, the emptier the global pipeline of parts and components circling the globe, which is meant to feed manufacturers and retailers all over the world. If the disruption continues, we may see many manufacturers, and maybe even retailers, suspending their operations as they run out of the key inputs they need.”

And ultimately, those businesses that reply on that global supply chain are at risk of going bust.

You can easily see how that can have a massive negative effect on the economy and the financial markets.

But it’s not only the supply side of the equation here that’s the issue.

Even if you could fix the supply chain so that all the companies are getting the parts they need… and all the retailers are getting the stock of goods they’re used to…

What if nobody wants what you’re selling?

“It’s a demand crash”

I saw an interesting Twitter thread from Derek Wallbank, a senior editor at Bloomberg.

Wallbank writes:

“I don’t think people appreciate that the coronavirus economic hit isn’t going to be solvable the same way most recent crises have been absorbed or handled. A short thread…

“Folks are very used to dealing with liquidity issues, or supply issues. This isn’t that. This is a crash in *demand*.

“Usual tools for dealing with supply side crashes, or liquidity crashes, are somewhat obvious. If liquidity, inject more. If supply, inject more.

“You can’t *inject demand* in the same ways. This should be obvious, but let me give you an example:

“Suppose you sell private jets, and you want to sell that jet to me. Well, I don’t want a private jet. I’m not a pilot, I don’t have time, I certainly don’t have the money, and where would I put the damn thing? So you cut costs. I still don’t want it. I wouldn’t if it was free.

“Literally, there is no conceivable way you could sell me a private jet right now, at any price, unless I could somehow make money by reselling it. I ain’t gonna buy one.

“That’s a demand problem. There is no demand (from me) and thus you (the jet co.) can’t sell me one.

“Now imagine you’re selling something a lot of folks use — airline tickets — and no one buys. Cut prices? Sure. Free bags? Lounge access? Maybe upgrade to more legroom seats? Sure, why not. But what if the issue isn’t cost? What if it’s that people don’t want to fly *at all*?

“That’s the difference between normal crashes and *demand crashes*. Your supply-side solutions don’t solve demand problems. Not if demand is zero.”

The airline business is an obvious example of something that’s hit by a drop-off in demand in the current climate.

People don’t want to – or are not allowed to – travel. And you can see that theme lasting a while.

Little wonder we’re already seeing casualties in the sector, such as the recent collapse of UK operator, Flybe.

IAG, owner of British Airways, Iberia and Aer Lingus, has also taken a big hit since people stopped flying.

But it’s not just airlines. The knock-on effect is far-reaching.

If people aren’t flying, they’re not staying in hotels, eating in restaurants, going to theatres or concerts or using taxi companies and so on.

Dharshini David, BBC Global Trade Correspondent:

“As major outbreaks spring up outside China, it is clear that it is not just global supply chains but also demand from consumers that’s suffering, as efforts to contain the virus keep them away from shops, bars and restaurants.

“What is unknown is exactly how bad and how lasting the impact could be. But what is known is that this comes at an already tricky time for the global economy with Japan, Italy, China and the UK among those already seeing growth faltering.

“As economists slash their growth forecasts, policymakers are debating how much they can do to help, given how low interest rates remain. What’s entirely clear is that investors face more anxiety ahead.”

Well, the Fed stepped up to the plate yesterday with what could be described as QE4.

After it slashed rates by 50 basis points last week and after the Bank of England followed suit this week, the Fed is upping its game.

It’s pumping $1.5 trillion of liquidity into the markets by buying US government bonds.

Not that it did much good for the overall market yesterday.

The Dow Jones and S&P 500 indices ended the day down 9.9% and 9.5% respectively.

It’s looking like the markets want more action.

Whether it’s slashing the Fed’s interest rate to zero that will do it… or the US government embarking on a huge fiscal stimulus programme… remains to be seen.

For now, let’s see if the relief rally that’s happening in world markets today can last.

Or whether investors will see it as another opportunity to sell the rally and get the hell out of the market.

Gold dragged down as investors cover losses

Meanwhile, look at our old friend, gold.

Yesterday, it too was chucked out as investors rushed to take profits to make up for losses elsewhere.

But this is not unexpected.

When you get an all-out rout as we’ve seen lately, gold can be taken down too.

But it tends to be a temporary setback. And when it recovers, it does so quickly.

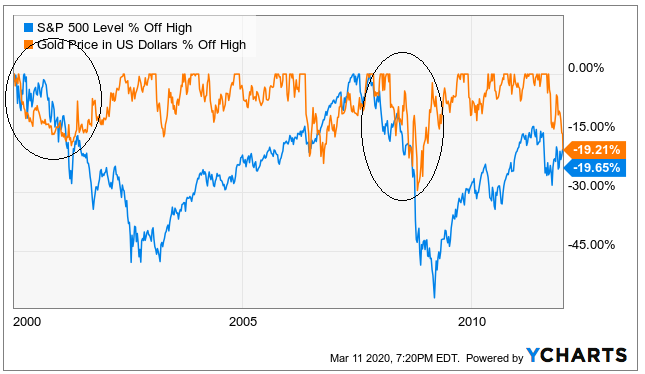

Lynn Alden of the Alden report:

“During the leading edge of the prior two recessions, gold sold off about 15% (2000) and 30% (2008). This is during the liquidity crunch.

“Gold then rallied to new all-time highs well before the S&P 500 recovered.

“This chart shows gold and S&P 500 percent drawdowns.

At the start of this week, gold was flying.

In dollar terms, it hit $1,703, up some 8% from the same time the previous week.

And that surge put it within 11% of its $1,891 all-time high set in August 2011.

But by the end of the week, it’s back down at $1,575.

From high to low, that’s a drop of 7.5%.

Still, if we step back a little and compare the performance of gold to stock markets, it’s still looking good.

Even over the space of just a week, gold’s 7.5% drop compares to a fall on the Dow Jones of 17.7% and 18.8% on the FTSE100.

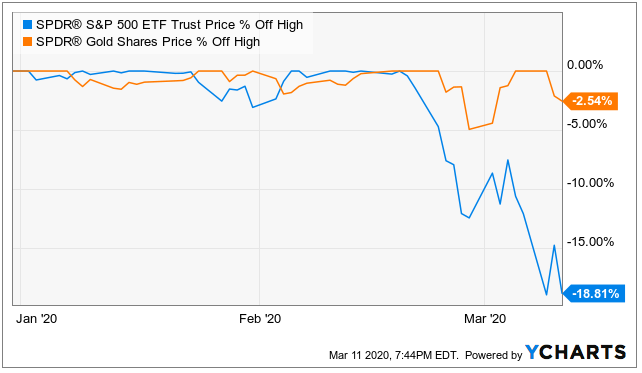

Here’s another chart from Lynn Alden.

It compares the performance of two exchange traded funds (ETFs). These are funds that aim to replicate specific indexes.

Here, Lynn looks at the SPDR Gold Shares ETF which tracks gold bullion.

And shows it up against the SPDR S&P 500 ETF, a proxy for the broad US stock market index.

She’s measuring the movement in both from the latest stock market peak in February.

And as you can see, gold has trounced stocks!

OK, since the market peak, the gold ETF gave up a little.

But nothing like what the stock market lost.

And that’s always our point about gold.

It’s not necessarily about making spectacular gains. (Although, those could well happen in the years ahead, in my opinion.)

It’s more about preserving value when traditional assets (i.e. stocks) are losing value.

And here you can see it’s served its purpose.

By the way, Lyn’s chart is a few days old. Since then, stocks and gold have fallen some more.

But it illustrates the point.

And gold is still far outperforming stocks… even after the metal has succumbed to profit taking.

The message remains: hold some gold.

And these sell-offs provide a decent opportunity to do so at a more advantageous price.

That’s my plan anyway: Buy the dips in gold.

As for stocks, it’s trickier.

I think we’re going to see a lot of companies going bust in the months ahead.

And even the ones that don’t, their shares could get a lot cheaper.

I’m not convinced we’ve seen the bottom of this market yet. The move from 11-year bull market to bear market has happened too quickly.

There could be a bigger sell-off to come before coronavirus is conquered.