What’s all this?

Stock markets have been marching higher again in April.

It looks like investors are buying into the whole global growth story.

It’s like they’re brushing off any threat of war: be it a global trade war, currency war, nuclear war…

… or an all-out assault on financial assets…

And piling back into the market as it rises.

But I’m not so sure that’s a good idea.

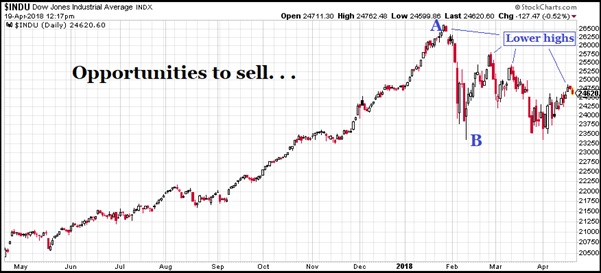

Short memories

These latest rallies in Western indices look to me more like an opportunity to sell than to buy.

Of course, people get comfortable when they see prices rising.

And so… they keep buying.

But they must have short memories.

Have they forgotten already what happened in February?

Here’s what it looked like back then for the Dow:

From the peak at A to the low at B that’s a 3,593-point collapse in the most widely followed stock market index in the world.

OK it’s not in crash territory.

But anything over 10% is a correction and this was a 13% move from the top.

And it happened in just seven trading days.

Of course, a sell-off like that can look like a great buying opportunity.

And anyone who backed up the proverbial truck and bought at the 6th of February lows must have been feeling pretty smug by the 27th.

The Dow surged 11% higher over those three weeks as buy-the-dippers piled in.

The line of least resistance is down

But ever since then, those gains have slowly ebbed away.

By yesterday’s closing bell, the Dow is just 6% up from the bleakest point in February.

And as we can see from the chart, the Dow’s carving out a path of lower highs.

That, my friend, is a down trend.

And the way I’ve been taught, you don’t fight the trend.

You go with the trend.

That’s the “line of least resistance” as Jesse Livermore called it.

That’s why I’d rather not be jumping on this latest April rally.

And by the way, it’s not just the chart that looks ugly to me.

Deep in debt

Have you read anything recently that sounds positive for the global economy and markets?

If so I’d like to see it.

Unless it’s more of the same drivel trotted out by the newswires.

Like this from Reuters:

“Robust business borrowing, rising consumer spending, and tight labour markets indicate the U.S. economy remains on track for continued growth…”

Good, so companies and private households are still living beyond their means rather than putting something away for tougher times.

That must be good for the outlook for the economy, right?

Well not according to the IMF:

“The world’s $164tn debt pile is bigger than at the height of the financial crisis a decade ago, the IMF has warned, sounding the alarm on excessive global borrowing.

“The fund said the private and public sectors urgently needed to cut debt levels to improve the resilience of the global economy and provide greater firefighting capability if things went wrong.”

If things went wrong…

But what could possibly go wrong?

Just count the ways

We’ve got the two largest economies in the world (the US and China) locked in trade negotiations that could escalate into a full-blown trade war.

And the third largest (Japan) also playing tough with Trump on trade.

We’ve got tension between East and West around the Syrian situation.

And North Korea.

And the rising oil price… rising inflation… rising interest rates… and the unwinding of quantitative easing (QE – one of the main drivers of asset prices for the past 10 years).

And we’ve lost another major force that was driving markets to all-time high after all-time high the past couple of years: the Big Tech stocks.

FAANG stocks (Facebook, Amazon, Apple, Netflix and Google) took a big hit in the middle of March.

Most were down between 10-15% in the second half of the months.

Until that point, they could apparently do no wrong.

And it was this gang of five super-stocks that was providing the momentum for the broader US stock market… and by extension global markets.

Big Tech could do no wrong.

They were ‘must-have’ investments and everybody wanted in on them.

And the market was pricing them that way, with rich valuations.

Pricey stocks are all well and good if sentiment is behind them and people want to keep buying.

But if the mood changes… they can and do fall fast.

Well, there has been a marked shift in sentiment, in no small part due to the Cambridge Analytica and Facebook data scandal.

And that’s hit the FAANG stocks and could well lead to them underperforming for the foreseeable future.

Worse still, if we get a serious decline in these Big Tech shares, it could well be a trigger for a wider bear market and even a sudden, brutal crash.

So, there’s plenty to be wary of right now.

Enough to make me feel a little cautious around stock markets.

I’m not looking to buy the dips right now…

Especially not when our old friend, Jamie Dimon, sounds such an ominous tone…

Fear of the unknown

Dimon, as you’ll know, is the top man at JPMorgan Chase, one of the biggest American banks.

Here at Monkey Darts we’ve had the odd dig at Dimon for his attacks on cryptocurrencies.

But he knows a thing or two about traditional finance and how markets work. So, he’s worth listening to on that score.

This from his annual letter to JPM shareholders:

“Since QE has never been done on this scale and we don’t completely know the myriad effects it has had on asset prices, confidence, capital expenditures and other factors, we cannot possibly know all of the effects of its reversal.

“We have to deal with the possibility that at one point, the Federal Reserve and other central banks may have to take more drastic action than they currently anticipate – reacting to the markets, not guiding the markets.”

I don’t know about any of that.

As Dimon says, none of us do.

But I can’t avoid one not-so-cheery thought…

If asset prices have been driven up to these sky-high levels primarily by QE… could the reversal of QE have an equal and opposite effect?

Like an all-out assault on financial asset prices…

If so, I certainly don’t want to be over exposed to the equity market.

And in such a scenario, safe-haven assets like gold and silver could well become the new ‘must-have’ investments.